Discover the top personal finance mistakes Indians must avoid in 2025. Learn how to manage money smartly, avoid debt traps, and build long-term wealth with practical, expert-backed tips.

💡 Introduction: Why Most Indians Struggle With Personal Finance

Despite earning well, many Indians end up with low savings, rising EMIs, and poor investments.

Why? Because financial education was never part of our school system.

In India, money mistakes don’t happen overnight — they grow over years of ignoring small financial habits.

This article reveals the 10 biggest personal finance mistakes Indians make, and how you can fix them to build lasting wealth.

💸 1. Living Without a Budget

A budget is your money map — without it, you’ll never know where your income is going.

Common mistake: Spending first, saving later.

Smart move:

- Follow the 50-30-20 rule — 50% essentials, 30% wants, 20% savings/investments.

- Use apps like Walnut, Money Manager, or ET Money to track expenses.

“If you don’t tell your money where to go, you’ll wonder where it went.”

🏦 2. Not Building an Emergency Fund

Most Indians rely on loans or relatives during crises — a huge mistake.

An emergency fund should cover 6–9 months of living expenses — rent, EMIs, bills, etc.

Where to park it:

- Liquid Mutual Funds

- High-interest savings account

- Short-term FD

💡 Pro Tip: Start small — even ₹2,000–₹5,000 monthly into a separate “Emergency” account.

💳 3. Overusing Credit Cards & Falling Into Debt Traps

Credit cards are useful — but dangerous when misused.

Mistake: Paying only the “minimum due” — leading to 36–42% annual interest.

Smart move:

- Always pay full due before the due date.

- Use credit only for planned, essential purchases.

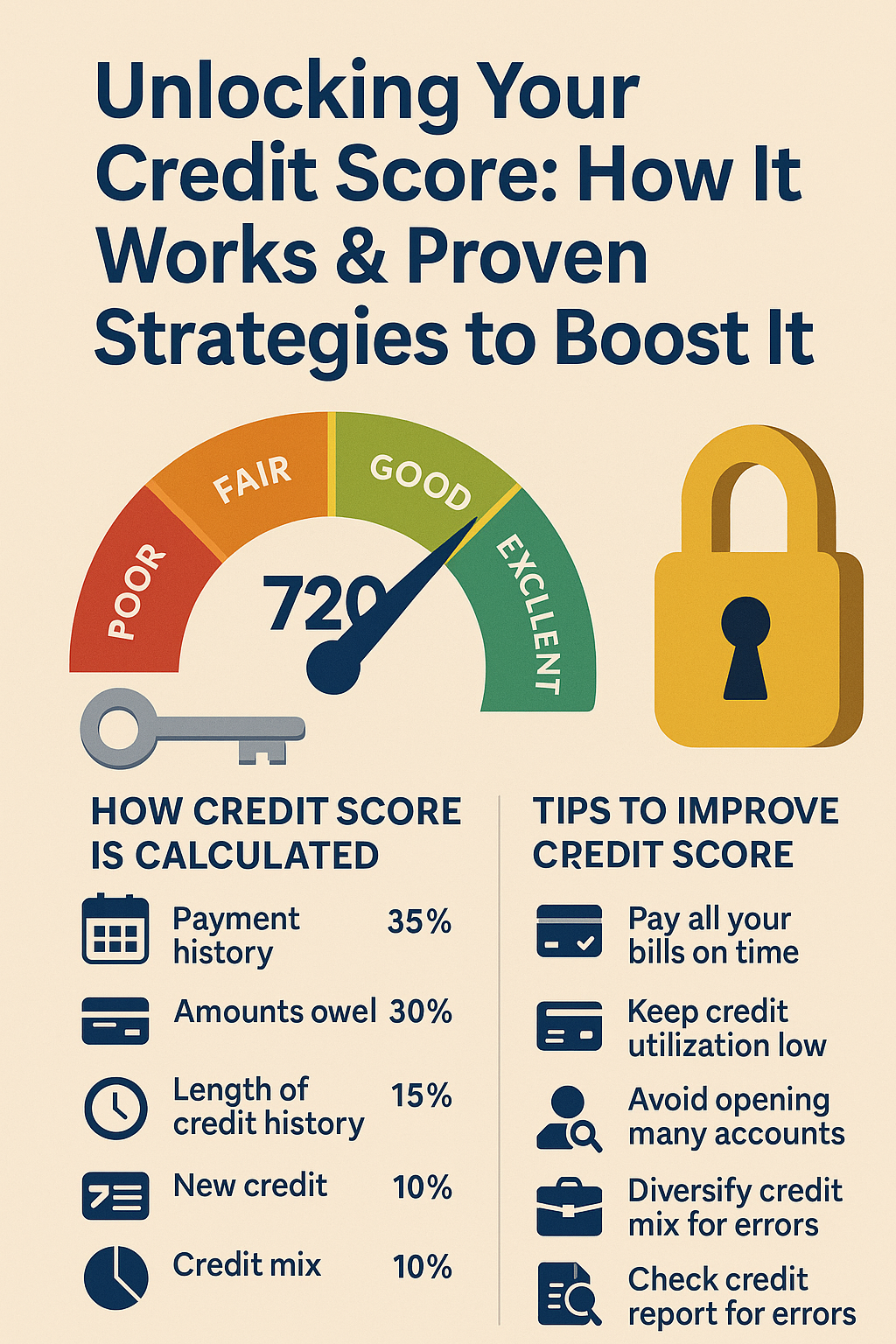

- Keep your credit utilization <30% to maintain a healthy CIBIL score.

🏠 4. Buying a House Too Early (or Too Big)

Homeownership is an emotional goal in India — but it shouldn’t come at the cost of your financial health.

Common mistake: Buying a property before building a financial base or taking huge EMIs (40–50% of salary).

Better strategy:

- First, create an emergency fund + term insurance.

- Aim for home loan EMI <30% of monthly income.

- Rent if necessary, invest the difference in mutual funds until ready.

💰 5. Ignoring Term Insurance

Many Indians buy expensive life insurance plans that mix investment + insurance — the worst combo.

Reality:

Your insurance should protect income, not promise returns.

Smart move:

- Buy a pure term plan covering at least 20x your annual income.

- Avoid ULIPs and traditional endowment plans unless needed for specific goals.

Best term insurance providers (2025):

- HDFC Life Click2Protect

- Tata AIA Sampoorna Raksha

- Max Life Smart Secure Plus

🏥 6. Skipping Health Insurance

Medical costs in India are skyrocketing — one hospitalization can wipe out savings.

Mistake: Relying solely on employer-provided insurance.

Smart move:

- Take a personal health policy for family.

- Choose ₹10–15 lakh cover with cashless network hospitals.

- Top-up with super top-up plans for extra coverage.

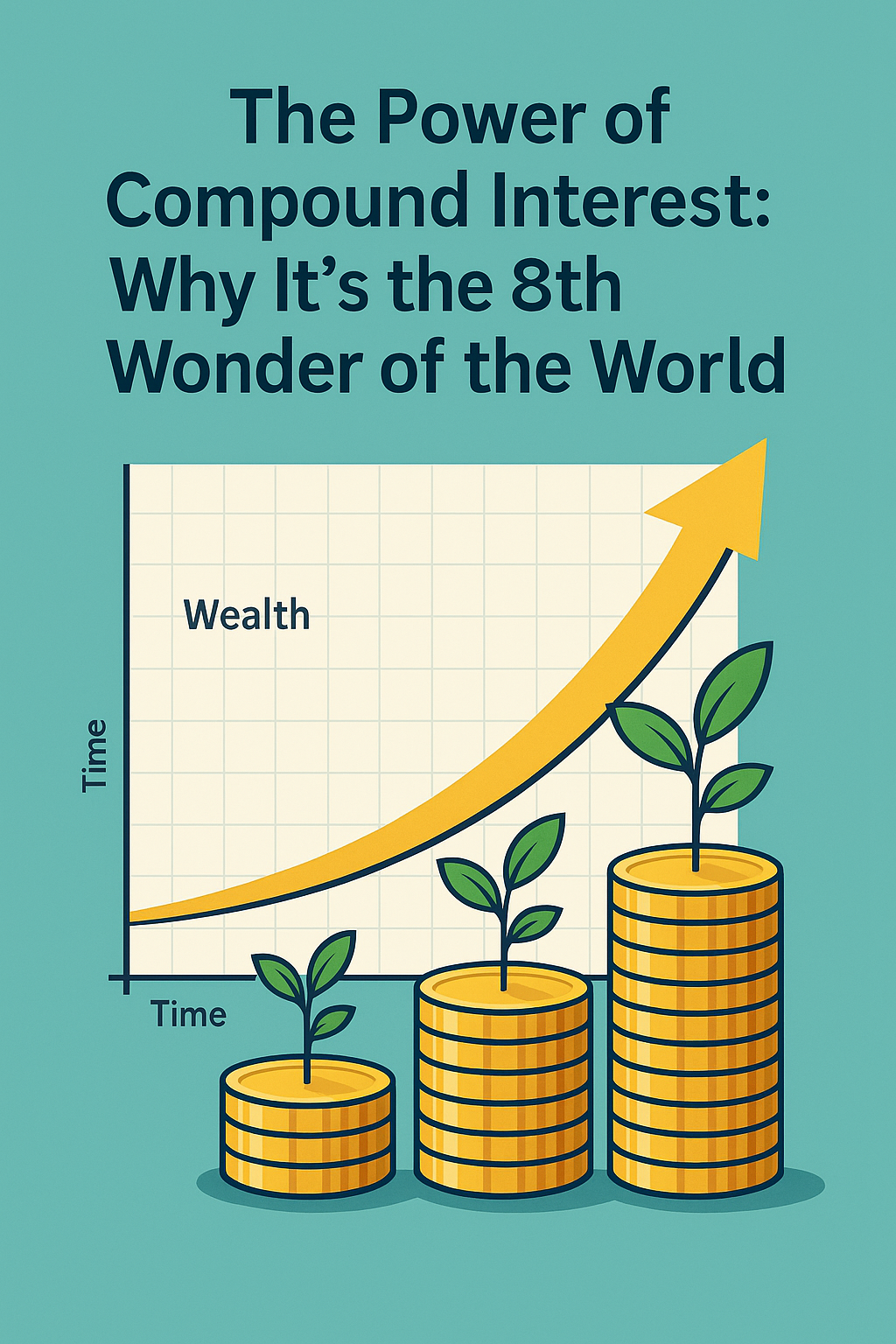

📊 7. Not Investing Early

The biggest mistake Indians make: delaying investments.

Waiting until your 30s or 40s means losing years of compounding.

Example:

- Start SIP at 25 → ₹5,000/month → ₹1.9 crore by 55

- Start at 35 → ₹5,000/month → ₹66 lakh by 55

Compounding rewards the early, not the rich.

Action:

Start a SIP today in a diversified mutual fund portfolio — even ₹500/month counts.

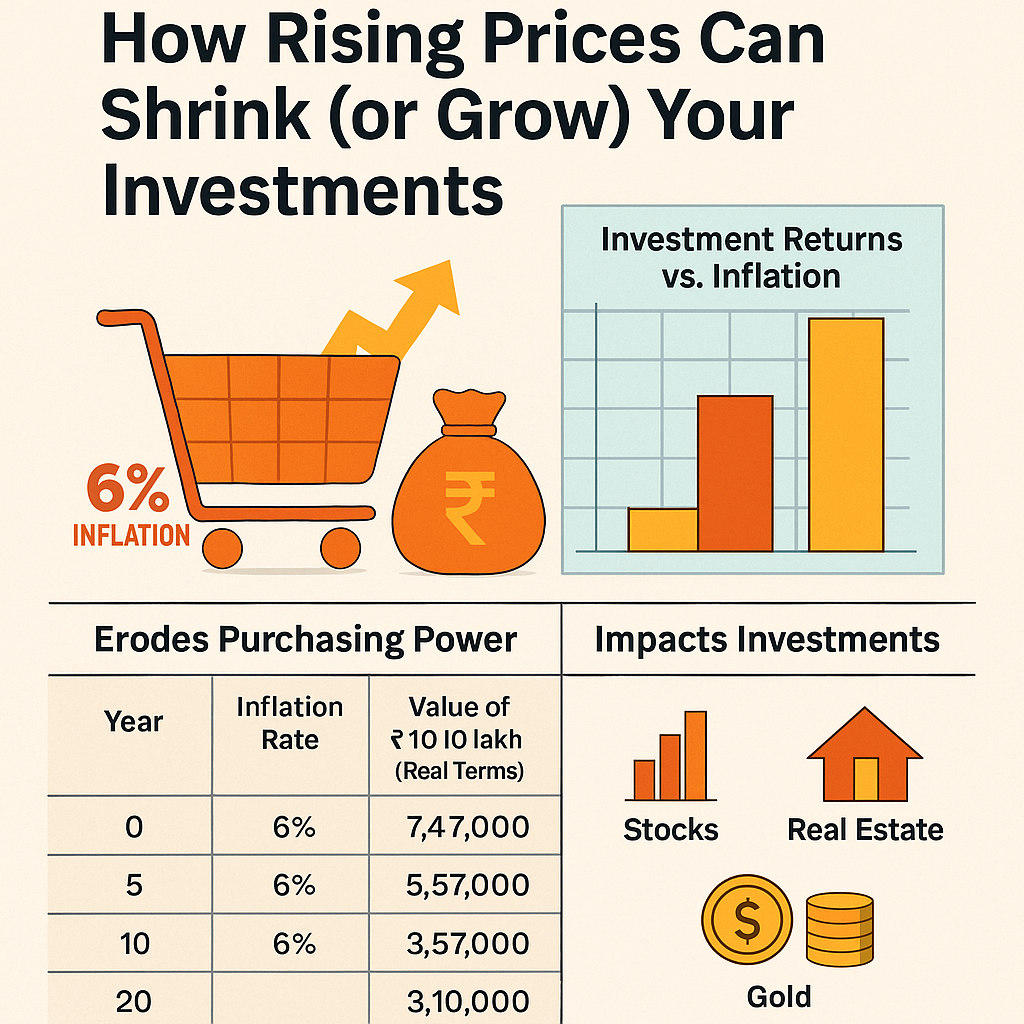

💵 8. Keeping All Money in Savings Account

Banks give ~3–4% interest — often below inflation.

Your money actually loses value sitting idle.

Instead:

- Invest in SIPs, debt mutual funds, PPF, or index funds.

- Keep only 3–4 months’ expenses in savings.

💳 9. Not Tracking or Improving Your Credit Score

Your CIBIL score decides your loan eligibility and interest rate.

Mistake: Ignoring credit score until a loan is rejected.

Smart move:

- Check credit score quarterly (CIBIL, Experian, etc.).

- Pay EMIs on time.

- Avoid multiple loan applications in short periods.

🧓 10. Ignoring Retirement Planning

Most Indians depend on children or pension schemes — risky in the modern economy.

Start early with:

- NPS (National Pension System) – market-linked growth + tax benefits

- EPF & PPF – safe, steady returns

- Mutual Fund SIPs – for inflation-beating wealth

💡 Goal: Build a retirement corpus covering 25–30 years of expenses.

🔁 Bonus Mistake: Not Seeking Financial Advice

DIY investing is fine — but lack of research can cost lakhs.

Consult a SEBI-registered financial advisor once a year to review your portfolio, tax plan, and risk level.

📋 Quick Recap: 10 Personal Finance Mistakes to Avoid

| # | Mistake | Smart Fix |

|---|---|---|

| 1 | No Budget | Track expenses with apps |

| 2 | No Emergency Fund | Save 6–9 months’ expenses |

| 3 | Credit Card Debt | Pay in full monthly |

| 4 | Buying House Too Soon | Keep EMI <30% income |

| 5 | Wrong Insurance | Choose pure term plan |

| 6 | No Health Cover | Get family health plan |

| 7 | Investing Late | Start SIP early |

| 8 | Idle Cash in Bank | Move to mutual funds |

| 9 | Ignoring Credit Score | Review quarterly |

| 10 | No Retirement Plan | Use NPS, PPF, MF SIPs |

🧭 Conclusion: Financial Freedom Begins With Avoiding Mistakes

Personal finance isn’t about earning more — it’s about managing smarter.

Avoiding these 10 money mistakes will:

✅ Protect your wealth,

✅ Improve cash flow,

✅ Reduce financial stress, and

✅ Build a secure future.

“Wealth isn’t built overnight — it’s built by avoiding mistakes every day.”

Leave a Reply